Bonds - Basics

By: Art Kamlet

A bond is just an organization's IOU; i.e., a promise to repay a sum of money at a certain interest rate and over a certain period of time. In other words, a bond is a debt instrument. Other common terms for these debt instruments are notes and debentures. Most bonds pay a fixed rate of interest (variable rate bonds are slowly coming into more use though) for a fixed period of time.

Why do organizations issue bonds? Let's say a corporation needs to build a new office building, or needs to purchase manufacturing equipment, or needs to purchase aircraft. Or maybe a city government needs to construct a new school, repair streets, or renovate the sewers. Whatever the need, a large sum of money will be needed to get the job done.

One way is to arrange for banks or others to lend the money. But a generally less expensive way is to issue (sell) bonds. The organization will agree to pay some interest rate on the bonds and further agree to redeem the bonds (i.e., buy them back) at some time in the future (the redemption date).

Corporate bonds are issued by companies of all sizes. Bondholders are not owners of the corporation. But if the company gets in financial trouble and needs to dissolve, bondholders must be paid off in full before stockholders get anything. If the corporation defaults on any bond payment, any bondholder can go into bankruptcy court and request the corporation be placed in bankruptcy.

Municipal bonds are issued by cities, states, and other local agencies and may or may not be as safe as corporate bonds. Some municipal bonds are backed by the taxing authority of the state or town, while others rely on earning income to pay the bond interest and principal. Municipal bonds are not taxable by the federal government (some might be subject to AMT) and so don't have to pay as much interest as equivalent corporate bonds.

U.S. Bonds are issued by the Treasury Department and other government agencies and are considered to be safer than corporate bonds, so they pay less interest than similar term corporate bonds. Treasury bonds are not taxable by the state and some states do not tax bonds of other government agencies. Shorter term Treasury bonds are called notes and much shorter term bonds (a year or less) are called bills, and these have different minimum purchase amounts.

In the U.S., corporate bonds are often issued in units of $1,000. When municipalities issue bonds, they are usually in units of $5,000. Interest payments are usually made every 6 months.

A bond with a maturity of less than two years is generally considered a short-term instrument (also known as a short-term note). A medium-term note is a bond with a maturity between two and ten years. And of course, a long-term note would be one with a maturity longer than ten years.

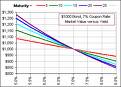

The price of a bond is a function of prevailing interest rates. As rates go up, the price of the bond goes down, because that particular bond becomes less attractive (i.e., pays less interest) when compared to current offerings. As rates go down, the price of the bond goes up, because that particular bond becomes more attractive (i.e., pays more interest) when compared to current offerings. The price also fluctuates in response to the risk perceived for the debt of the particular organization. For example, if a company is in bankruptcy, the price of that company's bonds will be low because there may be considerable doubt that the company will ever be able to redeem the bonds. When you buy a bond, you may pay a premium. In other words, you may pay more than the face value (also called the "par" value). For example, a bond with a face value of $1,000 might sell for $1050, meaning at a $50 premium. Or, depending on the markets and such, you might buy a bond for less than face value, which means you bought it at a discount.

On the redemption date, bonds are usually redeemed at "par", meaning the company pays back exactly the face value of the bond. Most bonds also allow the bond issuer to redeem the bonds at any time before the redemption date, usually at par but sometimes at a higher price. This is known as "calling" the bonds and frequently happens when interest rates fall, because the company can sell new bonds at a lower interest rate (also called the "coupon") and pay off the older, more expensive bonds with the proceeds of the new sale. By doing so the company may be able to lower their cost of funds considerably.

A bearer bond is a bond with no owner information upon it; presumably the bearer is the owner. As you might guess, they're almost as liquid and transferable as cash. Bearer bonds were made illegal in the U.S. in 1982, so they are not especially common any more. Bearer bonds included coupons which were used by the bondholder to receive the interest due on the bond; this is why you will frequently read about the "coupon" of a bond (meaning the interest rate paid).

Another type of bond is a convertible bond. This security can be converted into shares of the company that issues the bond if the bondholder chooses. Of course, the conversion price is usually chosen so as to make the conversion interesting only if the stock has a pretty good rise. In other words, when the bond is issued, the conversion price is set at about a 15--30% premium to the price of the stock when the bond was issued. There are many terms that you need to understand to talk about convertible bonds. The bond value is an estimate of the price of the bond (i.e., based on the interest rate paid) if there were no conversion option. The conversion premium is calculated as ((price - parity) / parity) where parity is just the price of the shares into which the bond can be converted. Just one more - the conversion ratio specifies how many shares the bond can be converted into. For example, a $1,000 bond with a conversion price of $50 would have a conversion ratio of 20.

Who buys bonds? Many individuals buy bonds. Banks buy bonds. Money market funds often need short term cash equivalents, so they buy bonds expiring in a short time. People who are very adverse to risk might buy US Treasuries, as they are the standard for safeness. Foreign governments whose own economy is very shaky often buy Treasuries.

In general, bonds pay a bit more interest than federally insured instruments such as CDs because the bond buyer is taking on more risk as compared to buying a CD. Many rating services (Moody's is probably the largest) help bond buyers assess the riskiness of any bond issue by rating them.

Picture: www.gummy-stuff.org

Related Links:

Bonds - Amortizing Premium

No comments:

Post a Comment